Magic of Log Returns: Concept – Part 1

- Eng Guan

- Mar 3, 2023

- 6 min read

Updated: Mar 10, 2023

Ever heard of the term log returns? No, it is not a written record of your fund performance or anything to do with a wooden block. But it is also nothing to fret about if this is the first time you hear of it. While log returns may be unfamiliar, most of us should have come across the mathematical term logarithm during school days. Except that back then, you are probably wondering why you would even need to know anything about this cryptic expression. I did not fully appreciate it until much later as well.

Making mathematics simple can be a rather challenging task. So when I started writing this article, I was thinking about whether I can just do away with explaining all the mathematical complexities and dive straight into how you can use log returns. In the end, I decided it is not going to look complete without some academic treatment on the topic. I know some will cringe at the thought of having to relive their school days again, but not to worry, I am more of a practitioner than a theorist, so I will try to make this as painless as I can.

Let’s Compound Away – Compound Returns

The logarithm function is inexplicably linked to the compounding function. To revisit the concept of compounding, let’s use a typical bank deposit example. If you put $100 in a bank with an annual interest rate of 10% and a yearly compounding period. What you get in a year can be expressed as follows:

Note that this formula is the same as the sum of a geometric series where

D0 is the initial deposit of $100

Dt is the value of the deposit at the end of the period

R is the 10% annual interest rate

n is the number of compounding periods per year which is 1 since we are doing yearly compounding

t is the total time period in years which is 1 year

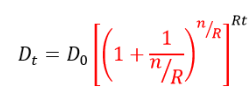

What if we increase n to 365 i.e. daily compounding? Then we would get

With a higher frequency of compounding, you ended up with $110.51558 at the end of the year. $10.51558 is the effective interest you make a year from compounding a 10% annual rate daily. This is more than the $10 in the yearly compounding scenario. Why? Because in a daily compounding scenario, you earn interest every day. And those interest, in turn, makes you more interest i.e. interest on interest.

A Special Case of Compounding – Continuous Compounding

So, what happens if we compound infinitely during the period? This is what we called continuous compounding. But, how do we even compute this? First, we have to re-express the equation in the following form:

It might take a while for you to figure out that this is the same equation. All I did was just a little manipulation. Why go through such a seemingly superfluous step? Because we need to get the expression highlighted in red. This red portion has a unique property. When n goes to infinity, the number within this red bracket magically converges to the Euler number called e which has a value of 2.7182818284590 …………… This is also the number used in your exponential function, and with it, we can further simplify our equation to arrive at a figure for a continuous compounding scenario:

Under continuous compounding, you will get an effective interest of $10.51709 or in percentage terms 10.51709%. The key takeaway at this stage is to know the relationship between effective interest and continuously compounded interest: (1) Effective interest rate – this is the interest you get as a proportion to the amount you put in and it depends on the frequency of compounding, (2) Continuously compounded interest rate – this is the interest rate that, when compounded continuously, gives you the effective interest rate for this scenario.

Now Let’s Log Away – Log Returns

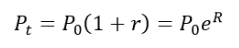

So how do all these relate to log returns? Let us now use stock prices instead of bank deposits to illustrate the concept.

P0 – Initial price of the stock

Pt – Price of the stock at the end of the period

R – continuously compounded rate over the period

r – simple return of the stock over time t

We can equate Pt as follows:

If you compare this against our earlier bank deposit example, you will notice that the simple return r is actually the equivalent of the effective interest, and R is the continuously compounded return needed to produce the simple return r during that period.

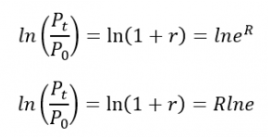

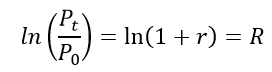

Dividing all by P0 and applying a special logarithm called the natural logarithm (ln) which uses the Euler number e as its base, gives us

The logarithm of a number that is equal to its base gives you a value of 1. So,

ln(1+r) is what we called the log returns. It is the same as R which is the continuously compounded rate of return that will grow the price of the stock from P0 to Pt.

Cool Stuff About Log Returns

There are a couple of interesting things about log returns.

1. Log returns can be added across time periods.

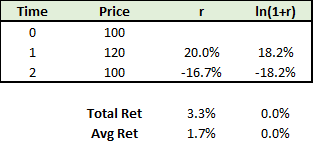

But adding simple returns, on the other hand, can lead to misleading outcomes. What do I mean by that? For example, let’s say you have a stock worth $100 that rose to $120 in the first time period and then goes back to $100 in the second time period. Going by simple returns, you will get a 20% increase in the first time period and -16.7% decrease in the second time period. If you just add them up or even take an average, you will get a total return of 3.3% and an average return of 1.7% even though you did not make any money at all. Log returns, however, being the continuously compounded return, can be added across time. Adding up the log returns over the period gives you a total and average return of 0% in this example.

If you want a little mathematical rigour:

The convenience of being able to use addition instead of multiplication makes manipulation in Excel a lot easier.

2. Log returns can be easily converted back into simple returns

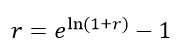

To get simple returns out from the log returns, you can easily do it by applying the exponential function.

3. Log returns follow a normal distribution

In the realm of asset pricing, stock prices are assumed to follow a lognormal distribution. Note that this is an approximation and not necessarily reflective of the actual distribution. But a lognormal distribution gives the desirable property to ensure that stock prices never go below zero. The stock price also seems to move in an exponential way over time. In addition, if the prices are lognormal distributed, then it follows that the log of its prices will have a normal distribution. And we know that log returns can be expressed in terms of stock prices (see the equation below). So log returns are normally distributed.

Not So Cool Stuff About Log Returns

1. Log returns are not intuitive

While log returns are more manageable, simple returns have the advantage of being more intuitive. When people ask you how much you make this year, your reply is going to be something along the lines of “Oh, I made 20%.” And that 20% refers to the simple return. You are almost never going to say things like “Oh, I make a continuously compounded 18.23%.” I mean who speaks like that? If the person who hears it flips out a calculator and starts keying the numbers, do not be surprised. Because that is actually a good sign. It means he understands what you are talking about.

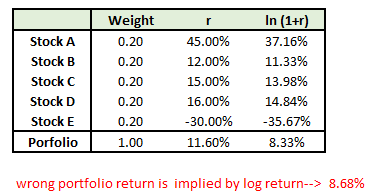

2. Log returns cannot be added across securities of a portfolio in the same time period.

If you managed a portfolio, you are almost going to have at least a few securities. The simple return of your portfolio over any time period is the weighted sum of all the simple returns from each of the security. However, you cannot pull the same stunt with log returns. It will give you an erroneous number. Remember that log return is a continuously compounded rate over time. When you add log returns, you compound. Across different stocks within the same time period, there is no compounding element here. So for computing portfolio return across contributions from securities within the same time period, use simple returns instead.

Concluding Part I

Here is the end of Part I or the more theoretical stuff. I have included an excel file: Log-Returns-Part-1.xlsx to illustrate some of the things I talked about here. It is very straightforward, so there is not much to explain. In Part 2 Magic of Log Returns – Practice, I will show more examples in Excel on how log returns can be used including one where I construct a performance table making use of log returns and a few other functions in Excel. It will give you a better appreciation, in particular as to why I say log returns make things easier.

See you soon!

Want to know more about AllQuant?

Comments