Beating Robo-Advisors In Their Game

- AllQuant

- Aug 23, 2023

- 6 min read

Updated: Aug 24, 2023

Imagine that you are a retail investor living in the 80s. One day, you stumbled across a time machine that transports you directly into the modern world. It would be the equivalent of finding yourself in an investment paradise. You are spoilt for choice. Services usually reserved for the rich are now readily available to the masses. This is often enabled by technology. One such service is the financial advisory service. Technology has allowed customized portfolio solutions to be implemented for many small clients simultaneously. Retail clients can start with a small amount and build up their nest egg by investing regularly. The term for such a service is robo-advisory.

The first robo-advisor launched in 2010 in the US, but the concept has since spread globally. Several robo-advisors have also sprouted in Singapore, and the top few have grown to manage more than SGD$ 1 billion. This is no mean feat considering the size of the market and the typical client profile. But other than the fact that retail clients can access the service, are the solutions offered by robo-advisors different from traditional wealth managers?

Asset Allocators At Heart

While some robo-advisors offer thematic portfolios such as "socially responsible", "green energy" or "artificial intelligence", the mainstay is still the good old asset allocation along the lines of modern portfolio theory. Clients will answer some questions during account opening to determine their risk profile. Based on their risk profile, the algorithm will recommend a certain asset allocation. A client that can take on more risk can have a higher allocation to equities. A client with a more conservative profile can have a higher allocation to safer assets such as government bonds for example. Another way, though we are not sure if it is implemented by local robo-advisors, is to have the same recommended asset allocation but where the risk level can be dialed up or down by adjusting the cash holdings. A client with a lower risk appetite will hold more cash while the highest risk taker will invest all cash into the recommended asset allocation.

Achilles Heel of Asset Allocators

Modern portfolio theory permeated the wealth management industry because of a powerful concept that works very well - diversification. Adding non-correlated assets into a portfolio can reduce risk without necessarily sacrificing returns. And even if returns are reduced, the corresponding risk reduction is significantly more, making it worthwhile. However, correlation is not static, making this the weakness of modern portfolio theory. When cross-asset correlation increases and becomes positive, the assets tend to move up and down in tandem, nullifying the effectiveness of diversification. This is exactly what happened in 2022 making it one of the toughest investing environments in history.

Correlation reached historical highs in 2022 before tapering off in the first half of 2023. But, it has come back up in recent months. It looks like we may be in for another challenging period.

Can We Be Our Own Robo-Advisor?

Now that we know that robo-advisors are mainly asset allocators, can we do it ourselves or DIY? To get the answer, we can do a backtest to see if the results match the typical robo-advisors. There are two big robo-advisors in Singapore. Without naming them, let's call them Robo A and Robo B. Robo A started in 2017 and only has one balanced portfolio, whereas Robo B started in 2018 and has a range of portfolios for clients to choose from. For Robo B, I will just use their conservative and aggressive portfolios for comparison.

For our DIY portfolio, let me build the following:

✅ For the equities component, I chose the iShares MSCI ACWI ETF (ACWI) which seeks to track the investment results of an index composed of large and mid-capitalization developed and emerging market equities.

✅ For the bonds component, I chose the Vanguard Total World Bond ETF (BNDW) which offers a broad, diversified exposure to the global investment-grade bond market.

✅ The target allocation will be 60% to ACWI and 40% to BNDW which is also the typical allocation recommended by financial advisors.

✅ I will rebalance this portfolio every month to bring the weights back to the 60-40 target.

✅ I factored in transaction costs inclusive of slippage.

✅ No leverage is employed.

Let's call this the Global Balanced portfolio. It can only start in 2018 because that is when BNDW was launched.

A simple observation of the results (see chart above) shows you that this portfolio tracks the robo-advisors' performance fairly well. So, yes, you can easily be your own robo-advisor. And operationally, it is not too difficult because there are only two ETFs, and you just need to rebalance them every month. Thus, the real value of a robo-advisor only comes in if you lack discipline and want an automated process to contribute a portion of your income into the portfolio using a dollar-cost averaging approach.

Can I Avoid The Achilles Heel?

You will notice in the comparison chart above that all the portfolios were hit badly in 2022, and they have yet to recover the losses. This is because most asset classes went down, and no matter how you allocate, there is nowhere to hide. Is there a way to avoid this? You can, but it requires more advanced strategies than just asset allocation. And these advanced strategies are not available in the typical robo-advisors, at least not yet.

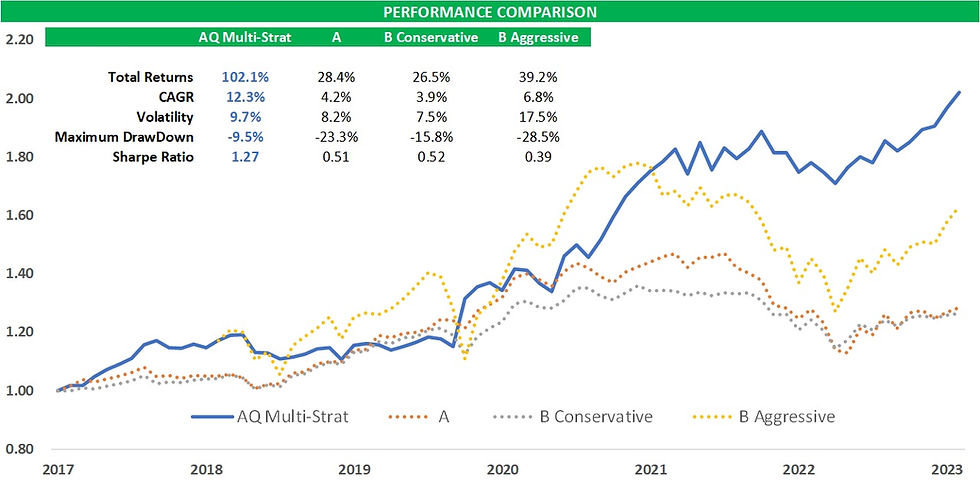

AQ Multi-Strategy Portfolio

Our AQ multi-strategy portfolio, which can be implemented with the help of Da Wei, an iFAST Global Markets (Singapore) senior investment adviser, not only diversifies across multiple assets, it also diversifies across strategies. A simple way to look at this is to visualize each strategy as an investment specialist. All of them are competent and profitable. But they specialize in different areas and they make money from the financial markets in different ways from each other. While one is undergoing a bad patch, another may be doing well or vice versa. And that is how as a team, they complement each other and become stronger than any individual alone.

If you take a snapshot of the portfolio, it can look like a typical balanced portfolio. However, there are a few important differences.

1️⃣ The portfolio holds volatility ETFs because of our volatility trading strategy. This is a unique strategy that offers a non-correlated return profile and can potentially act as a crisis hedge.

2️⃣ The portfolio can also switch out of an asset class totally and go into cash if the market environment is not favorable to that asset class.

3️⃣ The advanced sector allocation model can pick sectors well and can also size down and allocate to safe-haven assets or cash if necessary.

Because of the important differences above, the AQ multi-strategy portfolio can do better than a typical balanced portfolio over time (see chart below).

Implementing AQ Multi-Strategy Portfolio with IFAST Global Markets

In terms of convenience, it is not too different from using robo-advisors. The iFAST advisory process makes it easy for clients to implement the AQ multi-strategy portfolio in a hassle-free manner. In fact, there are some distinct advantages. Not only will you have an account under your own name with full visibility, but you will also retain full control. All trades that need to be done will be advised ahead of time and will only be executed with your approval. On top of that, a dedicated adviser (Ou Da Wei, Senior Investment Adviser from iFAST Global Markets) will see to your financial needs, a personal touch you will never find with robo-advisers.

Find out how you can implement AQ multi-strategy portfolio through a coffee session!

AllQuant brings to the table a new solution for busy professionals. We put all our 30 years of joint experience across asset management, banking, proprietary trading, and hedge fund to work. And we designed an actively managed multi-strategy model portfolio that is resilient enough to weather different market conditions.

You can now build such a portfolio through iFAST Global Markets without lifting a finger. In this collaboration, we are combining AllQuant’s expertise in hedge fund strategies and iFAST’s advisory capabilities and bringing it to your doorstep.

Ready to start your investment journey? Chat with us over a cup of coffee through a session facilitated by iFAST Senior Investment Adviser, Ou Da Wei, to find out more.

Disclaimer & Disclosure

We are not financial advisers or fund managers. The information published on this Site is provided for informational purposes only. It is not intended to be, nor shall it be construed as, financial advice, an offer, or a solicitation of an offer, to buy or sell an interest in any investment product. Nothing on this site constitutes accounting, regulatory, tax, or other advice.

Any performance shown on this Site is model performance and is not necessarily indicative nor a guarantee of future performance. You should make your own assessment of the relevance, accuracy, and adequacy of the information contained on this Site and consult your independent advisers where necessary.

AllQuant is carrying out introducing activities for iFAST Global Markets (Singapore) as an independent entity and is NOT an agent, servant, employee, representative, or in partnership with iFAST Global Markets (Singapore). AllQuant will be receiving remuneration or introducing fees from iFAST Global Markets (Singapore).

Comments